570 Credit Score: What It Means and How to Improve It

A 570 credit score can feel like a heavy burden, especially when you’re trying to qualify for a loan, credit card, or even rent an apartment. But here’s the good news: you can fix it. While it takes time and discipline, improving your credit score is completely possible if you follow a smart, step-by-step approach.

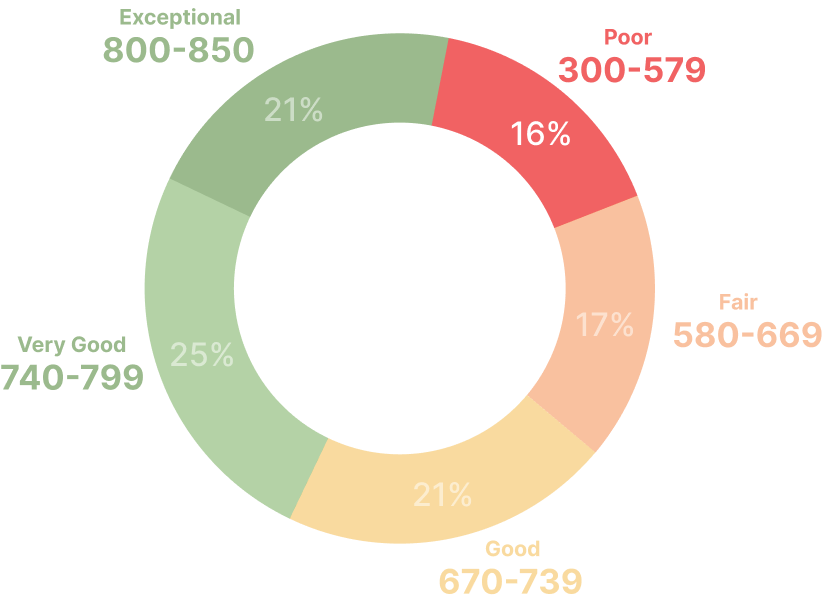

What Does a 570 Credit Score Mean?

A credit score of 570 is considered “Poor” under most credit scoring models, such as FICO and VantageScore, which typically classify scores from 300 to 579 in this category. This places you near the lower end of the credit score spectrum, indicating that lenders may view you as a higher-risk borrower.

As a result, you could face:

- Higher Interest Rates: Lenders may offer you credit but at much higher interest rates. This means borrowing money will cost you more in the long run.

- Loan Application Denials: You might find it difficult to get approved for credit cards, auto loans, mortgages, or personal loans—especially from traditional lenders.

- Larger Deposits: You may be asked to pay higher security deposits for utilities, cell phone contracts, or rental agreements.

- Lower Credit Limits: If approved for credit, your credit limits may be low, making it harder to manage credit utilization.

- Difficulty Qualifying for Premium Products: Cards with rewards, perks, or low interest rates often require at least “Good” credit.

But the good news is that a low score isn’t permanent—and with the right strategy, you can start improving it today.

Your Score Is Low—But Fixable Let CoolCredit’s AI Show You Exactly What To Do Next

Fix NowIs a 570 Credit Score Permanent?

The good news is: A 570 credit score is not permanent. It reflects your credit behavior at this moment in time—and that can change. By developing better financial habits, you can gradually move your score into the “Fair” and even “Good” categories. Many people improve their scores within 6–12 months by making consistent efforts.

How to Fix a 570 Credit Score?

Step 1: Check Your Credit Reports for Errors

The first thing you should do is review your credit reports from all three major credit bureaus: Equifax, Experian, and TransUnion. Mistakes on your report can unfairly drag down your score.

What to look for:

- Incorrect account balances

- Late payments that aren’t yours

- Accounts you don’t recognize (which may indicate identity theft or fraud)

- Closed accounts reported as open

- Duplicate accounts

How to do it:

You can request a free copy of your credit report from AnnualCreditReport.com. By law, you’re entitled to one free report from each bureau every year.

If you find any errors, dispute them immediately. You can file disputes online with the credit bureaus. Fixing even a small mistake can give your score a boost quickly.

Step 2: Pay Down High Balances

One of the biggest factors in your credit score is your credit utilization ratio—the amount of credit you use compared to your credit limits.

Best practice:

- Keep your credit utilization below 30% on all credit cards.

- If possible, pay off your revolving balances entirely to free up available credit.

Even paying down a portion of your balances can make a noticeable difference and show lenders you’re managing your credit responsibly.

Step 3: Catch Up on Past-Due Accounts

Your payment history accounts for about 35% of your credit score, making it the most important factor.

What to do:

- Bring all past-due accounts current as quickly as you can.

- Focus on the most recent delinquencies—they hurt your score the most.

- Once your accounts are current, make sure to pay all bills on time going forward.

This step is essential to stop further damage to your score and lay the foundation for improvement.

Step 4: Avoid New Hard Inquiries

Whenever you apply for new credit (like a loan or credit card), the lender performs a hard inquiry on your credit report, which can lower your score by a few points.

How to manage this:

- Limit your applications for new credit while you’re rebuilding your score.

- Only apply when absolutely necessary and when you’re confident you’ll be approved.

This helps you avoid additional drops in your score while you work to improve it.

Step 5: Consider a Secured Credit Card

If you’re struggling to get approved for traditional credit cards, a secured credit card is a valuable tool for rebuilding credit.

How it works:

- You make a refundable security deposit, which usually becomes your credit limit.

- Use the card for small purchases and pay the balance in full every month.

This allows you to build a positive payment history and show responsible credit use, which can gradually raise your credit score.

Step 6: Keep Older Accounts Open

The length of your credit history also influences your credit score. The longer your credit accounts have been open, the better.

Tips:

- Don’t close old credit card accounts unless there’s a compelling reason (like high fees).

- Even if you don’t use these accounts often, keeping them open adds to the average age of your credit history, which benefits your score.

Step 7: Monitor Your Progress Regularly

Improving your credit score is a gradual process—but staying informed helps you stay motivated and make adjustments as needed.

What you should do:

- Use free credit monitoring tools offered by banks, credit card companies, or financial apps.

- Track your score and watch for any unexpected changes.

Go From 570 to 700 Faster Than You Think With AI Powered Credit Repair

Get StartedWhy Improving Your Credit Matters?

Your credit score is more than just a number—it’s a key that opens or closes financial doors. Here’s how raising your score from 570 can make a real difference:

▪ Lower Borrowing Costs:

With a low credit score like 570, lenders charge higher interest rates because they view you as risky.

Even a modest increase to the "fair" range can reduce interest rates on loans and credit cards, saving you hundreds or thousands over time.

Example: On a $10,000 car loan:

- With poor credit (570 score), you might pay 15–20% interest

- With a fair score (e.g., 630), your rate could drop to 10–12%

That translates into lower monthly payments and huge savings over the life of the loan.

▪ Better Financial Products:

With a higher credit score, you get access to:

- Credit cards with rewards and perks

- Higher credit limits

- Lower fees

- Personal loans without a co-signer

At 570, your options are limited and often come with high fees or deposits (like secured credit cards). Improving your score gives you better choices.

▪ Higher Approval Odds for Rentals and Jobs:

Many landlords check credit when you apply for an apartment. A low score might mean:

- Getting denied

- Having to pay a higher security deposit

- Needing a co-signer

Some employers, especially in financial services or positions of trust, also review credit reports as part of their hiring process. A better score helps you look more reliable and reduces barriers.

Conclusion

A 570 credit score puts you in the “Poor” range, which can make life a bit harder when it comes to borrowing or qualifying for good rates—but it’s far from the end of the road. With consistent effort, like paying on time, reducing balances, and staying on top of your credit report, you can improve your score and open up better financial opportunities.

And if you want a little help along the way, an AI-powered credit repair app like CoolCredit can make the process easier, offering expert assistance to help you get your score moving in the right direction faster.

FAQs

Q: What can I get approved for with a 570 credit score?

A: With a 570 credit score, you may still get approved for secured credit cards, some personal loans, or subprime auto loans, but typically at higher interest rates and less favorable terms.

Q: How to fix a 570 credit score?

A: You can improve a 570 credit score by paying bills on time, reducing outstanding debt, disputing errors on your credit reports, and gradually building a positive credit history.

Q: Can I get a house with a 570 credit score?

A: Yes, it’s possible to get a house with a 570 credit score, especially with an FHA loan, but you’ll likely need a larger down payment and will pay higher interest rates.

Q: Is 570 an okay credit score?

A: A 570 credit score is considered poor, meaning it can limit your financial options, but it’s definitely fixable with consistent credit improvement efforts.