How to Pay Off Credit Card Debt: 5 Methods To Implement

Not sure how to pay off credit card debt? This blog has the answers you’re looking for.

Credit card debt often piles up quietly, and many people don’t even realise it until the balance feels overwhelming.

For instance, when you pay only the minimum amount due, most of that payment goes toward interest. As a result, the actual balance reduces very slowly. Small, everyday expenses like coffee, food delivery, or online shopping may not feel significant in the moment. Still, over time, they add up and start accruing interest if not paid in full.

In some cases, people end up using one credit card to pay for another, which only shifts the debt and increases the interest burden. Moreover, a single emergency expense placed on a credit card can linger for months longer than planned, turning a short-term fix into long-term debt. And then, missing a payment makes things worse.

Together, these factors cause credit card debt to grow faster than expected, even without any major or unnecessary spending.

However, there is a bright side. There are ways to pay off credit card debt. We’ve discussed some of the most effective options below.

Boost Your Credit Score the Smarter Way

Get StartedHow to Pay Off Credit Card Debt: 5 Proven Ways

In 2025, almost 28% of Americans reported falling deeper into credit card debt. If that sounds familiar, you’re not alone, and it’s not too late to fix it. Here are the best ways to pay off credit card debt.

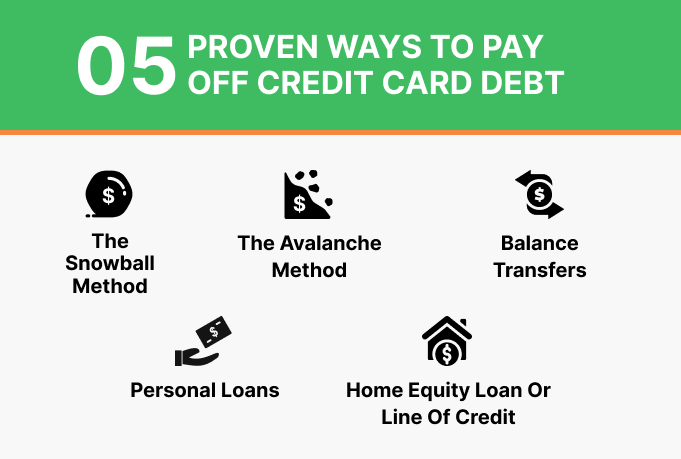

1. The Snowball Method

The debt snowball method focuses on small wins first. Simply, list all your debts from the smallest balance to the largest, regardless of interest rate. Then, continue making minimum payments on all debts, but put any extra money toward the smallest debt. Once that debt is fully paid, take the amount you were paying on it and roll it into the next smallest debt. This creates a snowball effect. Therefore, each payoff frees up more money to attack the next balance, helping you build momentum and stay motivated.

Pros:

One major advantage of this method is motivation. Paying off smaller debts quickly gives a sense of progress, which makes it easier to stay consistent. Also, it’s easy to understand and follow, requiring little financial calculation. Because it focuses on behavior rather than math, it especially works well for people who struggle to stay disciplined or feel overwhelmed by multiple debts.

Cons:

The biggest drawback is that it ignores interest rates, which means you may pay more interest overall compared to other methods. High-interest debts may remain unpaid for longer, causing them to grow faster. As a result, this method may be emotionally effective. But it’s not always the most cost-efficient way to eliminate debt.

2. The Avalanche Method

The debt avalanche method is a strategy for paying off debt that focuses on minimizing interest costs. Create a list of all your debts in order of highest interest rate to lowest, regardless of the balance amount. Then, continue making minimum payments on all debts, but direct any extra money toward the debt with the highest interest rate first. Once that debt is fully paid off, you move to the next highest-interest debt. Over time, this approach reduces how much interest accumulates and helps you clear debt more efficiently.

Pros:

This method simply saves you a lot of money. By targeting high-interest debt first, you pay less total interest over time and often become debt-free faster. Also, mathematically, it is the most efficient approach as it works especially well for credit card debt, which usually carries high interest rates.

Cons:

When you have a high-interest debt with a large balance, progress can feel slower at the beginning. This can be discouraging for people who rely on quick wins to stay motivated. It also requires a bit more planning and awareness of interest rates, which may feel less intuitive for some.

3. Balance Transfers

It is a way to pay off or manage credit card debt by moving an existing balance from one credit card to another. You can use a card that offers a low or 0% introductory interest rate for a fixed period (such as 6–18 months). This method to pay off credit card debt simply works on this logic - Instead of paying high interest on your old card, your payments during the promotional period go mostly toward reducing the principal. This can make it easier to catch up and pay down debt faster.

Pros:

The biggest benefit is interest savings. A 0% or low-interest period can significantly reduce how much interest you pay, allowing more of your money to go toward clearing the balance. It can also simplify finances by consolidating multiple credit card balances into one payment. For people with a clear repayment plan, balance transfers can speed up debt payoff and provide temporary relief from high monthly interest charges.

Cons:

Most balance transfer cards charge a transfer fee (typically 3–5% of the amount), which adds to your debt upfront. Moreover, the 0% interest is temporary. If the balance isn’t fully paid before the promotional period ends, interest rates may apply again. Approval often depends on the credit score, and opening new cards can impact your credit if not managed well. There’s also a risk of running up new debt on the old card after transferring the balance, which can leave you worse off than before.

4. Personal Loans

Using a personal loan to pay off credit card debt involves taking a single loan. It is usually with a fixed interest rate and fixed monthly payments. You can use that money to clear one or more high-interest credit card balances. This turns revolving credit card debt into an installment loan, making repayments more predictable and easier to manage.

Pros:

A key advantage is lower interest compared to most credit cards, which can significantly reduce the total interest paid over time. Fixed monthly payments and a clear end date provide structure and help with budgeting.

Cons:

Interest rates depend on your credit profile. If your credit score is low, the rate may not be much better than a credit card. Additionally, some loans come with processing fees or prepayment penalties, increasing the overall cost. Once the cards are paid off, there’s also a risk of running them up again. As a result, it can lead to even more debt if spending habits don’t change.

5. Home Equity Loan or Line of Credit

Honestly, if you’re thinking about how to pay off credit card debt, this option should come last. It’s important to avoid reaching a point where you have to put your home equity at risk.

A home equity loan provides a lump sum with fixed interest and fixed monthly payments. On the other hand, HELOC works more like a credit line, allowing you to borrow as needed, and it usually comes with a variable interest rate. Because these loans are secured by your home, interest rates are typically much lower than credit card rates.

Pros:

The biggest benefit is lower interest, which can substantially reduce the total cost of repayment. Fixed-payment home equity loans offer predictable monthly payments, making budgeting easier, while HELOCs provide flexibility to draw funds as needed. Consolidating multiple credit card balances into one loan can simplify finances and reduce monthly payment stress.

Cons:

The most serious risk is that your home is used as collateral; if you miss payments, you could face foreclosure. Moreover, closing costs, appraisal fees, and other charges can make this option expensive upfront. HELOCs often have variable interest rates, meaning payments can increase over time. There’s the danger of turning unsecured credit card debt into secured debt as well. Thus, if spending habits don’t change, you may end up with both credit card debt and a loan against your home.

Don’t Let Bad Credit Hold You Back

Try It NowKey Questions About Credit Card Debt—Answered

Figuring out how to pay off credit card debt is one thing. However, there are still a few widely held notions about credit card debt that need clarification, such as…

How Much Credit Card Debt is Too Much?

In general, credit card debt becomes “too much” when it starts controlling your choices instead of supporting them.

Moreover, it’s not just about the amount to be paid. It’s about how that debt affects your life, peace of mind, and ability to move forward financially.

If you’re only able to pay the minimum amount due each month, that’s a strong sign your debt is too high. Minimum payments mostly cover interest, so the balance hardly goes down and can take years to clear. Similarly, if you’re spending a large part of your income on credit card payments, it leaves little room for savings. Therefore, it means the debt is no longer manageable.

A major red flag appears when the answer to “How to pay off my credit card debt?” is “another credit card.” This often signals cash-flow pressure and a cycle where one debt is simply replacing another.

How Does Credit Card Debt Affect Your Credit Score?

In simple terms, a credit score tells lenders whether you’re handling credit responsibly or struggling to keep up. There are various factors to understand it.

First, it’s credit utilization. It means how much of your available credit you’re using. For example, if your credit card limit is ₹1,00,000 and you’ve used ₹70,000, you’re using 70% of your limit. High utilization signals risk to lenders and can lower your credit score. Even if you pay on time, carrying a high balance month after month can hurt your score.

Second is payment history. When you miss a payment or pay late, it negatively affects your credit score. Late payments are seen as signs of financial stress and can lower your score for years.

Lastly, high credit card debt increases the chance of default, which lenders closely watch for. If your debt keeps growing and payments become harder to manage, your score can fall sharply.

What to Do If You’re Unable to Pay Your Credit Card Bill?

If you’re unable to pay your credit card bill, the most important thing is not to ignore it. Try to pay at least the minimum amount due to avoid late fees and extra interest. If that’s not possible, contact your credit card issuer right away. They might offer temporary relief options like fee waivers or short-term payment plans.

Next, review your spending and cut back on non-essential expenses so you can free up cash. Moreover, avoid using the credit card for new purchases. If the debt feels unmanageable, consider structured options.

Conclusion

Credit card debt is too much when it stops being temporary and starts piling up. At that point, it’s a sign to pause, reassess, and look for answers to how to pay off credit card debt.

We recommend using the strategies outlined above to manage your credit card debt before it grows further. You can even combine multiple methods for the best results.

Once you start paying down your debt, CoolCredit can help you repair your credit at the same time. By reporting your on-time payments, CoolCredit helps boost your credit score, allowing you to tackle debt while rebuilding your financial health.

FAQs

Q: How Do I Avoid Getting Into Credit Card Debt Again?

A: To avoid getting into credit card debt again, keep your balances low, pay your bills in full whenever possible, and only use credit cards for expenses you can repay within the month.

Q: Are Credit Counselors Worth It?

A: Yes, credit counselors can be worth it if you’re feeling overwhelmed by debt. They help you create a realistic repayment plan and may negotiate with lenders on your behalf.

Q: Is My Spouse Also Responsible for My Credit Card Debt?

A: It depends. In most cases, your spouse is only responsible if they are a joint cardholder or if you live in a community property state.

Q: What Happens To Credit Card Debt When You Die?

A: When you die, your credit card debt is usually paid from your estate, not by your family. If there’s no estate or insufficient assets, the remaining debt is typically written off unless someone else is a joint account holder or co-signer.