What Is a Fair Credit Score?

Short Answer

589–669 is considered a fair credit score based on the FICO scoring model, while in the VantageScore scale, the “Near Prime” category with 601–660 is equivalent to fair credit scores.

Credit scores broadly range between 300–850 into different categories like poor, fair, good, very good, and excellent. If your credit score falls between 580 and 669, you are in the “fair” credit score category. In fact, 15% to 16% of Americans fall in this category.

But what does it actually mean? Your chances of getting approved for an auto loan, lease, mortgage, or new line of credit often depend on your credit rating. While lenders may consider a “fair” credit score, whether it's good or bad for you depends on where on the spectrum you are.

For instance, a landlord may consider a score of 600 ideal for renting on lease, but the same score may not be ideal when you want a car loan and the provider is accepting a 640 score or higher. While in both scenarios, your credit lies in the “fair” range, the particular scores can be either “good” or “bad” depending on your credit objectives.

Improve your fair credit score faster with AI-powered insights

Start NowLet’s break down the “fair” credit range for clarity and how different lenders perceive a fair credit score in different scenarios.

What Is a Fair Credit Score: Determined by FICO vs. VantageScore

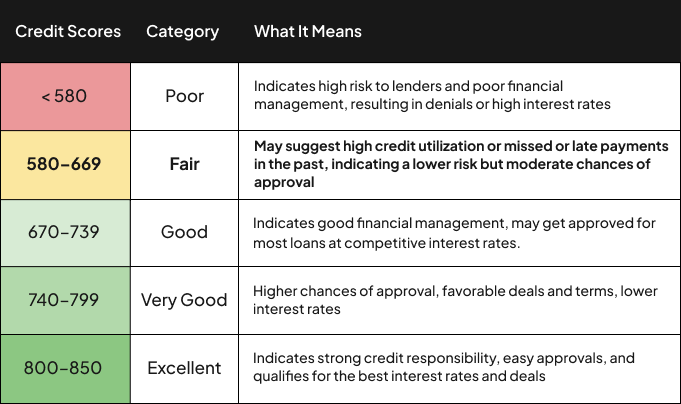

FICO credit scoring usually divides credit scores into 5 categories:

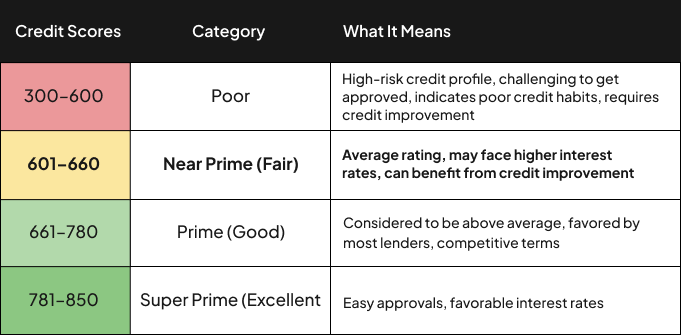

Whereas VantageScore divides credit scores into 4 key categories:

Percentage of People in the Fair Credit Range (580–669) by Age

| Age Group | % in Fair Credit Range |

| 18–27 (Gen Z) | 35% – 40% |

| 28–43 (Millennial) | 22% – 28% |

| 44–59 (Gen X) | 15% – 20% |

| 60–74 (Baby Boomers) | 5% – 8% |

What Does a Fair Credit Score Mean for You?

When your scores fall within a fair credit range, whether you are on the higher or lower end, it can have a significant impact. For example, we can categorize the range of "fair" credit scores as follows:

580 to 599

Lower on the spectrum

When your credit score falls below 600 in the credit score range, it is at the bottom end, which means lenders may view it less favorably. This leads to fewer approvals, limited borrowing capacity, qualifying ability for smaller personal loans, and financing options with higher interest rates. At this range, you are likely to qualify for secured credit cards.

600 to 619

Considered financially stable

In this range, whether your credit score sits at 601, 610, 615, or 619, this indicates improvement in your credit management abilities. Most lenders may view you as financially stable, and you may be able to qualify for unsecured credit cards, personal loans, and financing options, though interest rates may remain high as lenders may still feel cautious.

620 to 639

Better prospects for approval

Most lenders consider credit scores above 620 much more favorably. So whether your score is 621, 625, 628, 630, or 638, you can successfully apply for renting an apartment, a mortgage, FHA loans, auto loans, personal loans, and a new credit card. However, the interest rates may still be slightly higher than average, but you may unlock more prospective credit options.

640 to 659

Stronger financial stability

Borrowers with a 640+ credit score, including 642, 645, 648, 650, 655, 658, up to 659, are considered to be reliable by most lenders. At this stage, you may qualify for a broad range of financing options and loans and have a higher credit limit. Additionally, you can get competitive/lower interest rates and often favorable terms.

660 to 669

Improvement can lead to good credit

Credit scores like 661, 662, 664, 668, or 669 can help you get approved for new credit cards with rewards options, new loan options, better interest rates, and borrowing opportunities. Additionally, if your score is above 660, it means you are in the sweet spot where starting any credit-building efforts can boost your standing from “fair” to the “good” category. For instance, you can improve your credit scores with the CoolCredit app’s extensive credit monitoring and credit-building tools and features.

Ready to go from fair to excellent? Let AI guide your credit improvement.

Install NowHow to Improve a Fair Credit Score?

There are 4 key steps you can take to improve your credit scores:

- Make Timely Payments

A fair credit score usually signifies that you may have made late payments or missed a due date in the past. Therefore, it is crucial to never miss a payment going forward. Making timely payments over a long period of time can help improve your credit scores consistently.

- Lower Your Credit Utilization

When your credit-to-debt ratio is high, it indicates high credit utilization, which can lower your credit scores. However, when you pay off your debts faster and avoid applying for new credit too fast, or keep a gap of at least 6 months to a year before applying for new loans, this can significantly keep your credit utilization lower. Additionally, it's best to never max out your credit cards; ideally, use 30–40% of the credit limit to maintain credit utilization in a favorable state. A lower credit usage demonstrates better credit management to lenders.

- Pay Outstanding Balances

If your credit report features any outstanding balances left unpaid, it may be negatively affecting your credit score. It's best to negotiate an agreement and pay a lump sum for full settlement of such balances while you build your credit back up.

- Check for Errors in Your Credit Report

Sometimes the common errors in your credit report, such as misspelled personal details, inaccurate debt balances, loan dates, or other mistakes, may be lowering your credit scores. Also, look out for any fraudulent or suspicious charges on your credit report. It’s crucial to analyze your credit report carefully and file a dispute if you find any such errors.

You can raise a dispute from the official website of credit bureaus or use the CoolCredit app for personalized expert assistance to instantly file a dispute and maximize your chances of success. The app allows users to use AI analysis to flag all the negative items on their credit report and provides actionable steps and tools to resolve the issues.

Conclusion

A fair credit score between 580 to 669 can help you qualify for various financial products. However, it may feature limited borrowing ability and higher interest rates. It is not necessarily a setback but an opportunity to start building your credit. If you are in the “fair” category, there is room for improvement, and cultivating habits such as paying bills on time, resolving outstanding debts, lowering your credit utilization, and consistently building financial stability can help you move up to the “good” credit score category. Additionally, apps like CoolCredit can help simplify your credit repair/improvement journey by providing AI-backed insights, regular credit monitoring, and personalized tools to help strengthen your credit profile over time.

FAQs

Q: What Is Considered a Fair Credit Score for an Auto Loan?

A: Most auto loan providers accept 620 or 640+ as a fair credit score.

Q:What's a Fair Credit Score to Buy a $400k House?

A: For a conventional mortgage, a credit score of 620 or higher is usually required, but a 580 credit score can be acceptable for an FHA loan.

Q: Is 635 a Good Credit Score?

A: 635 falls into the fair credit score category (580–669), which is generally considered ideal for a range of credit products, including mortgage, personal loan, auto loan, credit cards, and more.

Q: Is 500 a Fair Credit Score?

A: No. 500 is considered a poor credit score, as scores falling below 580 are categorized in the “Poor” category. Scores above 580 up to 669 fall under the “Fair” category.

Q: Is 607 a Fair Credit Score?

A: Yes. 607 is a fair credit score, which signifies a moderate-risk credit profile. It can reflect that the borrower is becoming financially stable and working on improving their credit.